The UK’s changing demographic will create a number of challenges for employers, but perhaps the most pressing will be the need for organisations to help employees understand the realities of living longer.

If you read nothing else, read this…

- Older employees may choose to work because they enjoy their job, not because they can’t afford to retire.

- An ageing workforce requires employers to rethink the make-up of their benefits.

- Workforce planning should be about employees’ skillsets, not their age.

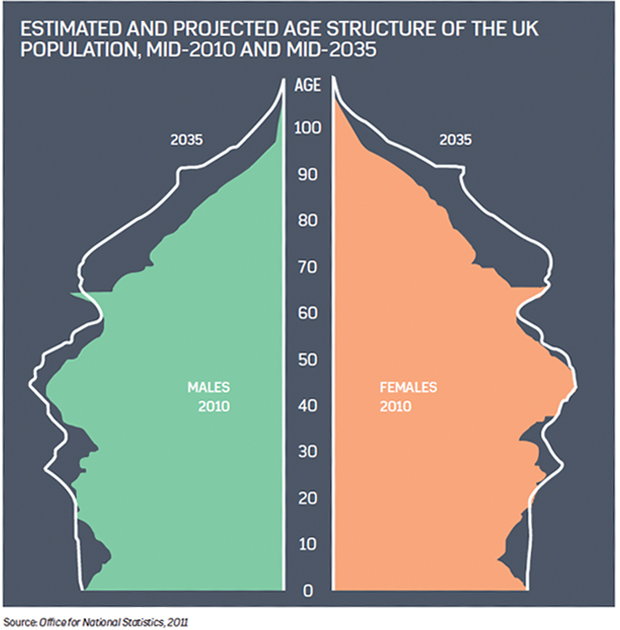

Employees aged over 50 make up 27% of the UK workforce, and by 2020 that proportion is expected to rise to one-third, according to the Department for Work and Pensions’ report Employing older workers , published in February 2013. For many employees, this will mean having to save more of their income into a pension scheme to be able to afford to retire.

Pensions auto-enrolment is helping to educate staff about the need to take responsibility for their own retirement income and save at least the required minimum contribution of 1% of salary into their pension.

But the downside of the legislation, introduced in October 2012, is that it is creating a false sense of security, with many employees believing that pension scheme membership alone will automatically give them an adequate pension pot at retirement. Employers therefore have their work cut out to educate staff about their finances.

Jo Thresher, head of money at work at benefits consultancy Jelf Group, says: “It’s about employers educating employees that [the minimum contribution of] 1% isn’t enough, and just because they’ve been put in a pension scheme doesn’t mean they’ve got a pension; it probably means they’ve got a pot of money that’s not worth very much.”

Employers could, of course, increase their own contribution levels, but this is not an easy proposition for HR and benefits professionals to pitch to their finance directors and fellow board members, particularly at a time when the world is just climbing out of recession.

Darren Philp, head of policy at The People’s Pension, says auto-escalation may be a more palatable proposition for employers’ boards to digest. This involves part, or all, of an employee’s future pay increases being paid automatically into their pension fund.

“As employees start getting pay rises, they might be encouraged to put a proportion of that into their pension and save for the longer term,” he says. “I think we’ll hear more about this in the coming years.”

However, Philp warns that auto-escalation puts an onus on employers, and HR and benefits professionals to provide workplace financial education and management programmes to help staff understand the importance and implications of increased savings in the context of their desired lifestyle in retirement and the level of savings required to achieve this.

Product development

But Britt Hoffman, head of DC at pensions consultancy P-Solve, says the defined contribution (DC) pension market first needs to overhaul itself to ensure employees’ pension savings are working as hard as possible to optimise their investment returns.

For example, the requirement for DC assets to be priced on a daily basis needs to be addressed because it is preventing scheme members from reaping the rewards of investing in a diversified range of assets, including higher-yielding, illiquid assets such as property.

“It’s about trying to close employees’ funding gap,” says Hoffman. “Everyone is familiar with [employers’ funding] deficit when it comes to defined benefit [DB] pensions, but actually that deficit is just as real for DC scheme members.”

Hoffman says pension providers need to apply diversification and a more active approach to pension fund asset allocation. She suggests applying the sophisticated investment techniques used by DB scheme providers, such as using financial instruments to hedge risk, to DC schemes to help optimise employees’ investment returns, enabling them to retire when they wish.

Flexible working

But employers also need to consider how to support staff who want to continue in employement simply because they enjoy working.

This may require supporting staff to restructure their pension to reflect their longer working lives. But it may also call for employers to rethink employees’ job roles in the context of their health and ability, as well as flexible working for employees who want a phased retirement and to work fewer days each week.

David Sinclair, assistant director, policy and communications at the International Longevity Centre, says: “One of the big problems we have with the current system is that lots of employees suffer when they go from working full-time to not working at all.”

Providing information about volunteering opportunities near employees’ homes is one way employers can help to support older workers who, as well as needing to build support networks where they live, also typically seek more meaningful types of work as they get older, says Sinclair.

“By giving employees a slow way out of the workforce and into their community through a phased approach to retirement, employers can keep staff longer and help pass on skills,” he adds.

Succession planning

Sinclair thinks that the changing demographic of the UK workforce will see savvy employers focus on transferring skills between different generations of employees, rather than on simply helping older workers to retire to make room for younger talent to come in.

“If an employer’s most promising employee is 68, a rational organisation has to make the most of that person’s skill,” he says. “Employment should be about ability, not age.”

Sinclair says HR and benefits professionals have historically used the default retirement age (DRA) as an excuse for not managing age-related issues in their workforce, such as the need to train underperforming employees who are approaching retirement.

“Getting rid of the DRA means employers have to start doing performance reviews properly and become a lot more age neutral,” he says. “This creates huge challenges in terms of skilling-up managers to manage people a lot older than them.”

Health management

Managers also need to be educated about how to support older workers in managing their health, and to recognise health-related issues that may affect their ability to perform in their job. These may include impaired vision and hearing, as well as musculoskeletal problems.

Employers’ occupational health teams can help to support older workers to remain fit for work, as can employee benefits. But employers may need to review their benefits package to ensure it addresses the needs of older workers. This may involve extending healthcare benefits to include health screening , optical and dental check-ups , as well as physiotherapy.

The International Longevity Centre’s Sinclair says: “There is a big role for HR professionals in terms of age management and working out how they manage this. Is there a different package they might want to offer older employees?”

With careful planning and employee input throughout, it is possible for employers to create a cost-effective age management strategy that both staff and finance directors can agree on. But employers need to take immediate action to address the issues at hand.

Case study: Employees’ skillsets underpin University of Lincoln’s workforce planning strategy

The University of Lincoln faces a number of challenges in managing its ageing workforce, particularly in terms of talent management.

Ian Hodson, reward and benefits manager, says: “Universities are an interesting case because the point of academia is to bring in new thinking or research, which often means we must ensure we have the capacity to allow for new staff.

“Also, in an academic context, an employee’s subject area is often their personal interest rather than just a job, so retiring means much more to them than not coming to their desk the next day.”

The university carefully manages its workforce planning strategy to ensure it has the right talent to deliver its business objectives by focusing on employees’ skillsets rather than their age.

For example, ongoing budget cuts in the university sector have driven the University of Lincoln to recruit staff with financial management skills. “This was never a massive requirement for staff in higher education because it wasn’t a priority,” says Hodson. “But now we find we are looking for staff who have those skills because that’s what we need. That’s not about age, but about us, as a business, identifying the need to bring in those skills.”

As well as natural staff attrition, the university creates the headroom required to recruit new talent through an intern programme that it launched two years ago. “We have made room for the skillset that generations Y and Z bring, very much around technology and different ways of thinking, by running the programme alongside the core workforce,” says Hodson.

The university also operates a role review process to underpin any organisational restuctures that are required. “While we can’t always create extra headroom for additional roles, we have a very prominent role review process, which managers can use to help them identify which aspects of a role and which competencies need to change,” says Hodson.

Meanwhile, the university is expanding its benefits offer to support older workers by providing financial education and healthcare benefits, such as health screening.

Hodson expects organisational restructures to become increasingly common as employers strive to recruit new talent into ageing workforces while complying with age discrimination law.

Viewpoint: Richard Wilson: Employers must help staff plan for retirement

The last 12 months have been hard work for HR and benefits professionals in dealing with pensions. Many have had to set up a scheme to prepare for auto-enrolment, or revamp their existing pension to make it more appropriate for their workforce.

But employers’ focus on pensions and retirement will not end when they reach their staging date and implement auto-enrolment. Their next challenge is to help older workers who are approaching retirement.

With the state pension age rising and employers no longer able to compel staff to retire, more employees will be working for longer, and many will have a more gradual transition from work to retirement. This makes it even harder for staff to plan, and even more important for them to secure a good deal in converting their pension pot into a retirement income.

Currently, savers lose up to £1 billion a year by not getting the best annuity deal. Employees will need support to stand any chance of deciding on the right plans and buying the best annuity, and employers must consider whether the help they currently offer is enough.

Realistic expectations

Employers must also consider whether their auto-enrolled staff are engaged enough and have realistic expectations. In October 2013, the National Association of Pension Funds conducted research with newly-enrolled scheme members, publushed in its Automatic-enrolment report, one year on . Most employees agreed with auto-enrolment and were relieved to be saving at last, but there was a realistic awareness that they were not saving enough, with 60% saying they were likely to save more in the future.

But, of course, this will not happen unless employers facilitate it. Employers that want their staff to be able to afford to retire will want to help them put more aside, perhaps with escalating contribution levels or higher matching rates.

Whatever employers’ approach, they must be mindful of the fact that getting staff into a pension scheme was always going to be the first step in a long journey to making sure they have a good outcome at retirement.

Richard Wilson is defined contribution (DC) pensions and investment policy lead at the National Association of Pension Funds

I quite like the styles.

my website – http://onlinesmpt200.com

Surprisingly user friendly website. Enormous info available on few clicks on.

My Website – http://iupatdc5.org

You have got very well thing these.

My Website – http://iupatdc5.org

You’ve one of the best online websites.

My Website – http://ts4arts.org/sales/

Wow, lovely website. Thnx …

My Website – http://as3nui.com/generic-viagra-best/

The material is very unique.

My Website – http://piccombo.org/cheap/

Wonderful images, the shade and depth of the pictures are breath-taking, they draw you in as though you belong of the composition.

my website – http://journal-cinema.org/

Passion the website– very user pleasant and great deals to see!

My Website – http://journal-cinema.org/

say thanks to a lot for your web site it aids a great deal.

My Website – http://journal-cinema.org/