Young people who delay saving for a pension until they reach middle age could lose up to £100,000 in employer pension contributions and tax relief, according to research by pension consultancy Barnett Waddingham.

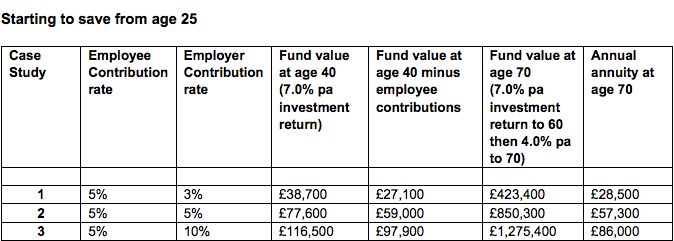

The research found that a 25-year-old, earning £25,000 per year, who delays joining a generous workplace pension scheme (with a 10% employer contribution rate) until they are 40 years old, could miss out on £97,900 of employer contributions, tax relief and estimated investment returns in addition to their own contributions.

The research also showed that an employee who had not saved into a pension scheme until the age of 40 could halve the value of their potential pension fund and subsequent income on retirement.

But those saving from age 25 into a generous workplace pension scheme could amass a pot of £1,275,400 at age 70, while those saving at age 40 would, in the same scenario, have a pension pot of £608,200.

Malcolm McLean (pictured), a consultant at Barnett Waddingham, said: “This research shows just how much a young person could lose by delaying the start of their pension plan by fifteen years.

“The message that many young people should take on board as the government’s programme of auto-enrolment continues is that this is an opportunity to receive some tangible help in planning a better future for themselves.”

Source: Barnett Waddingham

kate spade handbags louis vuitton bags outlet wholesale nfl jerseys christian louboutin uk http://www.patinsudouest.com/north_face.html http://www.iaetjournals.com/mulberryuk.html ??? http://graduates.sgu.ru/scripts/prada.html

http://www.sicbsikkim.com/nfljerseys8.html

http://www.iup.com/nfl-2.html

http://spacefold.com/custom_nba_jerseys_cheap.aspx

http://www.heroscharity.org/images/goyard.html

http://www.trobophoto.com/nfl6.html

http://www.patinsudouest.com/north_face.html

http://www.patinsudouest.com/north_face.html

http://www.leavittmachinery.com/nlf-5.html

http://www.daveagema.com/louisvuitton-outlet.html

mulberry710bagsS