This article has been supplied by Scottish Widows.

September saw the launch of Scottish Widows’ fifth annual Workplace pensions report, providing insight on the attitudes and behaviours of thousands of employees in relation to their workplace saving.

Two years on from the first auto-enrolment (AE) staging date, the impact that AE is having on workplace saving is starting to filter through. The success of the AE story is largely reflected in the proportion of employees now saving adequately for retirement. The research shows that 53% of respondents fell into this category. Not only is this a significant increase from last year (45%), but it represents the highest figure since 2009.

This is an encouraging landmark for auto-enrolment, but it also highlights a potential challenge for employers in the future.

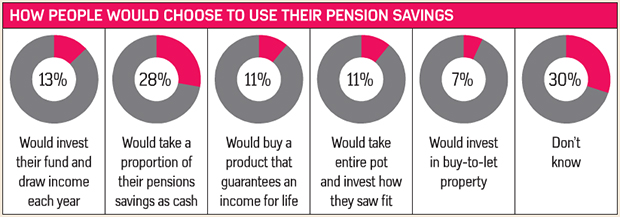

The Budget reforms announced by Chancellor George Osborne back in March have ensured that individuals will have significantly more choice in relation to what they do with their pension savings than ever before.

So, with AE ensuring that more employees are saving more money into their pension, and the Budget reforms ensuring that they have more choice about what they do with that money, the inevitable consequence will be that an increased number of employees will have some important financial decisions to take in the future when dealing with their pension pot.

So how will this impact employers?

With the at-retirement landscape becoming more complicated for workers to navigate, a number (17%) of employees will turn to their employer for guidance on the topic.

One crucial element of the Chancellor’s announcement was the promise of the introduction of a guidance guarantee providing individuals with information and support to better equip them to make the necessary decisions about their retirement saving.

The report also highlights the various sources currently cited by workers as points or reference for information on pensions. The Money Advice Service, which will not be involved in delivering the guidance, but will be part of an implementation team supporting the development of the website, is top of that list which suggests that many will readily take up the guidance guarantee. However, as one in six workers will be looking to their employer for help and support in this matter, the provision of this type of education and support is something that employers should be considering.

Perhaps reassuringly, almost half (49%) of respondents felt they would be comfortable managing the pensions, investments and savings that they have accumulated for themselves. And those aged 55 or older are more likely than any other group to feel that way, suggesting that those closer to retirement are significantly more engaged with their pension planning.

However, the big gap in this master plan is those workers in their 30s and 40s.

Auto-enrolment is doing an excellent job of bringing workers into pension saving for the first time, and the guidance guarantee will help support those getting closer to retirement, but for those somewhere in the middle what can be done to ensure that they are making the most of their long-term saving?

Again, engagement with workers throughout their careers on financial matters is something that employers might wish to consider. For many, the workplace is a natural channel through which to tackle these issues and many advisers and providers already offer access to workplace savings platforms providing workers with financial education and guidance.

Ultimately, employees’ level of engagement with their long-term saving will be key in determining what they can expect in retirement, and employers are uniquely placed to offer support to staff whatever their stage in the retirement planning journey.

Lynn Graves is senior manager, corporate pensions at Scottish Widows