Need to know:

- Financial worries can affect sleep, increasing the risk of mental and physical health problems, pushing up absence and potentially causing safety issues.

- Segmenting a workforce can make financial education more targeted and effective.

- Employers should not overlook simple changes, such as making it easier to claim expenses or promoting the budgeting tools provided with a workplace pension.

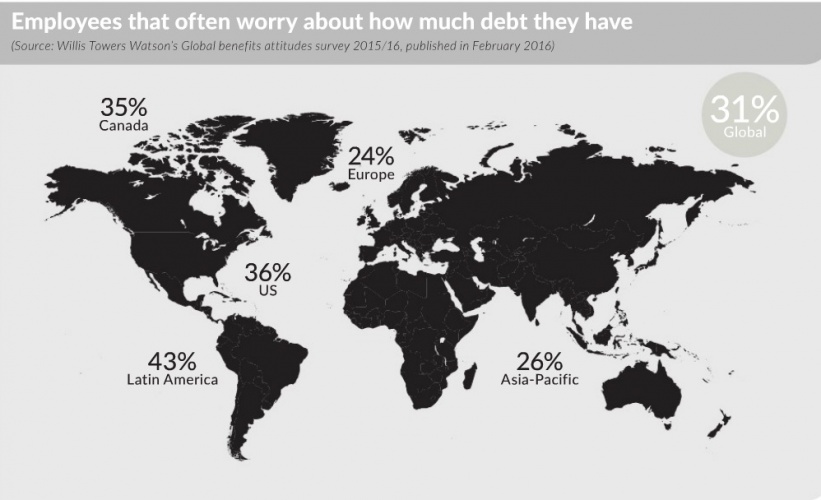

At some point most of us have struggled to make our salary last from one pay day to the next. But, for many employees, financial worries can have a significant effect on their health and wellbeing, with serious implications for employers.

Research by Mercer, published in November 2015, found that 78% of employee respondents feel that financial concerns contribute to stress levels. The research also found that financial worries have a negative impact on motivation (57%), energy levels (51%), as well as their overall health (46%).

Financial worries can have a major impact on an employee’s health and wellbeing, says Dr Mark Winwood, clinical director of psychological health at Axa PPP Healthcare. “If you’re worried about money, it can affect your sleep, which can then have knock-on effects on both physical and mental health,” he says. “Among the health implications are increased risk of colds and flu but also a greater risk of mental health issues such as depression and anxiety. It’s hardly surprising that suicide rates increase when there’s a financial downturn.”

Workplace woes

These health risks manifest themselves in the workplace through increased absence but also presenteeism. For example, on average, an employee suffering from poor sleep will cost a business around nine days a year in productivity, says Winwood. There can also be workplace safety issues if someone is not feeling 100%.

It is also important to note that money worries can affect all employees, not just the low paid. Annette Cox, associate director at the Institute for Employment Studies, says: “Financial wellbeing is about knowing how to manage your money. We’re faced with so many financial choices these days that it can be overwhelming.”

For example, the shift from defined benefit (DB) to defined contribution (DC) pensions; the increased choice at retirement as a result of pension freedoms; and the announcement in March’s Budget of a Lifetime individual savings account (Isa) that can be used to save for a home or towards retirement all present individuals with greater choice.

Giving employees the information they need to make informed choices is key to improving financial wellbeing, says Paul Bloomfield, business development director at Aon Employee Benefits. “Financial education can help people understand their choices and make better use of what’s available,” he explains.

Financial focus

Although financial education has been around for years in the workplace, under the financial wellbeing banner it takes a much more focused approach. For example, when Aon implements financial education programmes, the first thing it does is understand the needs of the workforce, says Bloomfield. “We’ll run focus groups and speak to employees to find out what the issues are,” he says. “You can’t just dive in with a session on retirement. You need to segment the workforce to ensure the programme is relevant.”

This targeted approach is also used by Nudge Global in its financial wellbeing programmes. Tim Perkins, director at Nudge Global, says: “We link into an employer’s benefits or payroll system to gain insight into its employees. This gives us information such as when they have a change in pay, status or address so we can deliver relevant financial education to them.”

For example, during Free Wills Month in March 2016, Nudge Global identified employees over the age of 55 with dependants and sent them details outlining what was available and how much people could save. “It has to be in the moment to get the most impact,” adds Perkins.

Building a programme

While it is possible to buy in education and other tools, many organisations may find they already have many of the components to support a financial wellbeing programme in place. Jeanette Makings, head of financial education at Close Brothers Asset Management, says: “Many employers will have an employee assistance programme with access to debt counsellors but you can also find budgeting tools on pension and savings plans. Making employees aware that this support is available can make a big difference.”

It is also sensible to look at some of the processes that may be in place within the workplace. This could include checking that day-to-day activities such as claiming expenses and overtime are as simple as possible to ensure that employees are able to benefit, says Bloomfield. “If these are too complex, people don’t claim,” he explains. “This can contribute to someone’s financial worries.”

A cultural change may also be necessary. “As a nation, we’re incredibly uptight about discussing money, especially in the workplace,” says Cox. However, turning this around is not always easy.

As well as making it easier to claim expenses and so on, employers can approach this by ensuring their benefits programme supports financial wellbeing.

This could include keeping any literature as simple as possible, with links to further information and tools where possible, but also including products that will be relevant to every employee. For example, rather than just offering a group self-invested personal pension and a corporate Isa, employers could offer savings products and competitive loans to help those employees who might not be ready to invest for the future.

Ultimately, offering a financial wellbeing programme to employees can be instrumental in helping to change the culture. “Start out with it as part of a broader health and wellbeing strategy, at least until discussing money becomes more acceptable,” says Cox.

Victrex uses segmentation to assist financial education

Victrex uses segmentation to assist financial education

Global high-performance polymer manufacturer Victrex employs around 600 people in the UK in roles ranging from manufacturing to management. When Sally Knill joined as head of reward in 2013, it soon became apparent that a financial education programme was needed. “There was limited appreciation of the benefits on offer,” she says. “The pension trustees were looking to change this but the two-hour-long seminar they proposed was far from engaging.”

Instead, Knill segmented the workforce by age and arranged for more life-stage focused workshops to be rolled out. As well as highlighting the benefits on offer, these workshops provided employees with information about everything from student loans to retirement options and spotting financial scams. “Knowledge increased significantly and we also saw a lot of employees using this to take out additional voluntary contribution (AVC) schemes to top up their pensions,” she says.

A year later, Knill introduced a broader health and wellbeing strategy, which included financial wellbeing, and decided to build on the success of the programme. “We were closing our defined benefit pension scheme to future accrual so we wanted to provide more financial education to ensure employees understood the new scheme and were able to take advantage of it,” she explains.

Taking the same segmented approach as before, but adding in one-to-ones for employees requiring more detailed guidance, the new programme had huge take-up and some very positive results. Just one employee has opted out of the new scheme with the majority choosing to pay in the 5% contribution the organisation was targeting. “Helping our employees make informed decisions about their finances is incredibly important for their wellbeing,” adds Knill.

“This also translates into business benefits such as higher employee engagement and lower turnover. Financial education definitely deserves its place in the employee benefits mix.”

Viewpoint: Understand the risks facing staff to get the support mix right

Viewpoint: Understand the risks facing staff to get the support mix right

Mental health is a universal attribute. We all have it, good or bad. We all experience times where we are at our best in work and at home, and we can all think of times when we felt at the edge of coping, or beyond. When we invest in our mental health, or the mental health of the staff that work in our organisations, we invest in those individuals, their families, and in the productivity of the workplace, whatever its mission.

In an operating environment where business needs to be both lean to weather financial turbulence, and attractive and competitive to retain and acquire talent, the support package that exists for staff is critical to attracting the best, and fostering a culture of early access to support, rapid return to work and effectiveness for staff who experience distress, be that arising from life events like bereavement, or from mental health problems such as depression or bipolar disorder.

Businesses provide a range of financial, physical and emotional wellbeing offers for employees. Getting the mix of these right is a challenge best met by understanding the risks faced by staff, the needs framed by the operating environment of the business, and the priorities staff express via engagement activities.

Increasingly, we are seeing that focusing on improved mental health as an outcome can provide a unifying theme to support packages. These usually involve early access to evidence-based treatment or information, direct support to mitigate the effect of absence and loss of earnings, vocational rehabilitation for physical injury or illness that should include the psychological impacts, or anonymous support for concerns with family, relationships, debt and housing. All of these are major factors in mental health.

Mental health can be the thread that brings together support across a business, to ensure a compassionate response to distress, rapid access, and return to work and all the benefits that can bring to an organisation and to an individual.

Chris O’Sullivan, programme lead, business development and engagement at the Mental Health Foundation.