New rules on how financial advisers and benefits consultants can be paid will have significant consequences for both employers and employees.

IF YOU READ NOTHING ELSE, READ THIS…

- Commission to advisers selling pension and investment products was banned on 31 December 2012.

- Employers can still pay for corporate pensions advice out of employees’ contributions through consultancy charging, but only in certain circumstances.

- Demand for financial advice, education and information is likely to soar as banks and IFAs service only rich clients’ business.

New Year’s Eve 2012 saw the dawn of a new era for the delivery of financial advice in the workplace that will have a significant impact on both employers and employees.

Since 31 December, financial services providers have been banned from paying commission on pensions and investment products, bringing to an end a system that has for decades seen the intermediaries selling products, including independent financial advisers (IFAs), brokers and advisers, taking a margin out of the deal.

The aim of the new rules, introduced by the Financial Services Authority (FSA) under the retail distribution review (RDR), is to stop intermediaries making biased product recommendations based on which provider pays the most commission.

This will affect employers and employees in different ways. Employers face having to sign a cheque for at least some of their advisory fees, while staff face reduced access to seemingly ‘free’ advice. This is because, until now, much workplace financial education has been provided by intermediaries’ commissions. Consequently, workplace financial planning information as an employee benefit is expected to become increasingly sought-after.

The RDR introduces two new ways for advisers to be paid for what they do out of funds held in products: adviser charging and consultancy charging.

Adviser charging is for situations where a financial adviser is advising an employee on a one-to-one basis, for example giving face-to-face pensions advice in the workplace. Under adviser charging, the IFA and the employee agree the fee, which is deducted from the product recommended on an ongoing basis.

This could, for example, be by way of a monthly deduction from the employee’s pension contributions, or could be a one-off deduction from a lump sum invested or the employee’s pension pot. Individual advice can cost between £75 and £250 an hour.

Consultancy charging is for situations where corporate pension advisers give employers advice on workplace schemes. Here, the adviser agrees with the employer the level of charges for services delivered and how these are to be paid, usually a percentage of the employer and/or employee contributions into a pension for a fixed period.

Ann Flynn, head of corporate marketing at Standard Life, says: “Consultancy charging is one way an employer can get access to quality financial advice.”

Contribution-based payment

As with commission-based payments in the past, consultancy charging allows employers to pay an adviser to do some, but no longer all, of the work it does in managing a corporate pension scheme out of the employees’ and/or employer’s contributions, rather than through a cheque from the employer.

The RDR will have no direct impact on employers that have always paid their pension advisers a fee for consultancy services in setting up and overseeing pension schemes.

But it will mean a massive change for employers that have not paid up front for financial advice, but have had their pension schemes implemented on the basis that the pension provider has paid commission to its employee benefits consultant or IFA.

Financial advice was never free under the old commission system, although it may have felt like it to some employers and employees.

Instead, pension providers charged a higher annual management charge (AMC) and paid commission to the adviser out of the extra revenue they received. This meant employees were ultimately paying the adviser’s fees through annual reductions in their pension pot.

Under consultancy charging, staff are told exactly how much they are paying an adviser.

But some government bodies are concerned about how much can be taken out of an employee’s pension pot through consultancy charging, and what it can be used for.

According to the FSA, consultancy charging deductions that take an individual’s contributions below the minimum required by auto-enrolment will not be permitted.

Consultancy charging ban threat

The Department for Work and Pensions (DWP) has threatened to go even further and ban consultancy charging altogether. Last November, just five weeks before the new RDR rules were due to take effect, the DWP launched a review of consultancy charging because of its concerns that advisers could take large deductions from employees’ pots. The review is not likely to be completed for several months, which means employers will be faced with tough decisions about consultancy charging just as the clock ticks down towards their auto-enrolment staging date.

Flynn says: “The landscape is becoming clouded by these interventions, which is unfortunate given how close so many employers are to their staging dates. Employers will have to speak to their advisers about what can be done on a consultancy charging basis and then agree a fee for the rest of the work.”

The Pensions Regulator (TPR) has also expressed concern over what consultancy charging should and should not be used to pay for. It has said consultancy charges should not be used to select and set up workplace pension plans, which would have to be paid for by a fee.

Flynn says ongoing expenses, such as default fund oversight, derisking as retirement approaches and member communications, could be paid for through consultancy charges.

In the past, some financial advisers have given individual advice to anyone in the pension scheme who wanted it, paid for out of the AMC of the whole scheme. This involved some element of cross-subsidy, with those with larger pots subsidising those with smaller ones. This is no longer possible for new schemes, but for schemes that were already set up on a commission basis before 31 December 2012, providers can still pay commission.

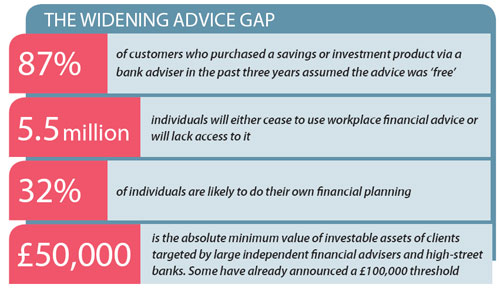

Robin Hames, head of marketing at Capita Employee Benefits, thinks it likely only those with large pension pots will be prepared to pay for full financial advice through adviser charging. “This is because until you have about £100,000 in your pension pot, it is questionable whether the value of the advice is worth its impact on the value of the fund,” he says.

Unsurprisingly, the abolition of commission is expected to transform the wider financial advice market, which could, in turn, increase significantly the value placed on money guidance, education and assistance offered as an employee benefit.

Bridging the advice gap, a report published by Deloitte in November 2012, concluded that the RDR would have two key effects: banks and IFAs will target only high-net-worth individuals, and some consumers will refuse to pay a fee for financial advice. These two factors will result in 5.5 million people ceasing to receive financial advice in future, according to the report.

Demand for more advice

Jacqui Holmes, a senior consultant at Towers Watson, sees the RDR adding momentum to a demand for more advice that has been growing for some time. “The increase in demand from employees for financial advice started a long time ago with the switch from defined benefit (DB) to defined contribution (DC) pensions and the introduction of flex,” she says.

“We are also seeing increased demand for information around the reduced lifetime and annual allowances for pension contributions, particularly where there are DB schemes in place, because this is now impacting lower income groups of employees.”

But Holmes argues that employers do not want to get involved in delivering regulated financial advice, preferring to offer education and information.

This view is echoed by Charles Cotton, performance and reward expert at the Chartered Institute of Personnel and Development. “Employers may get nervous about wanting to get involved with giving advice to their employees because if they get it wrong, there is the question of who carries the can,” he says. “They will, however, feel more relaxed about more general communications.”

Some financial services providers see this growing thirst for financial knowledge in the workplace as an opportunity for the distribution of their products and have been developing online financial planning tools and education materials as a more cost-effective way to guide employees towards making the right financial decisions.

But Towers Watson’s Holmes says these solutions are yet to take off . “We have been looking at the development of corporate platforms and take-up has been slow, in part because of the economic backdrop and auto enrolment,” she says.

Standard Life’s Flynn adds: “Auto-enrolment has made pensions a focus for employers for some time now, but we are seeing employers come back to the idea of widening their benefits proposition, and we expect more of this in 2014.”

And if Deloitte’s prediction of 5.5 million people being cut off from financial advice is correct, maybe things are about to change.

Case study: Roche finds right formula to raise financial awareness

Roche Pharmaceuticals is running a series of financial awareness seminars in both the pharmaceuticals and diagnostics parts of its business in conjunction with consultancy Towers Watson.

Doug Ross, HR manager at Roche Pharmaceuticals, says: “One of the themes that leapt out of the survey we did of our workforce was that employees wanted guidance on financial matters. There is a growing awareness that, in these times of austerity, everyone is having to look at their finances more generally. “

As a result, Towers Watson is conducting one-hour presentations on financial issues to groups of employees and Roche is holding drop-in sessions for people who want to talk about more personal matters away from a group situation.

The presentations will be filmed and the content will be made available on the web in chunks, so Roche’s workforce out in the field can also access it. “Take-up [of the sessions] has been dramatic and I believe staff see this as a very helpful service,” says Ross.

Roche also provides independent financial advice for its senior managers who earn more than £100,000.